MEETING TRANSCRIPT:

Greetings from Chicago Mid-Plains and team. This has Ben Buckner with AgResource Company in Chicago. Once again, more than pleased to join your annual meeting to help the farming community, which is what we strive to do at AgResource with our vision for the future in terms of supply and demand and price. Maybe, unfortunately, we are looking for a very different market landscape, at least in the second half of 2023, compared to what we’ve seen over the last 24 months recently. This bull market has been very exciting, but it has been intact for two full years now, and we’re starting to see we’re at a point in this bull market cycle where supply issues are being solved.

Generally speaking, the invisible hand is at work. In certain markets, we are seeing demand destruction. We are encouraging acreage expansion in Brazil, much like 2013 and 2014. We think that if Mother Nature cooperates, we could be building global grain and oil seed stocks pretty quickly. Maybe supply issues are just solved in one marketing year even, if Mother Nature is very kind to the principal in Midwest, Europe, and Black Sea region this spring and summer.

Our big picture themes too are really identifying the differences between this year, this winter, and last winter and spring when we were embarking on this period driven by fear of shortages and we did not know as a world whether we would have enough food and food products to get by to meet domestic global consumption. But that too I think has changed. We’re not seeing the same fear in the marketplace currently, and I think that makes good sense given how markets are evolving. The biggest thing that happened, I think, in the first half of 22 was the existence of interest rates. After 15 years of the cost of borrowing money being zero, now it does cost money to borrow money.

Thinking about the return on investment, just 12 months ago, all you had to do was beat 0%. You could borrow money at zero, put money into agricultural futures or other markets. As long as you had any kind of return at all, you were in the money. Now, we have to beat four, five, and 6%. People have been a little more picky about where those resources are allocated to. We also don’t think that the Federal Reserve is done raising interest rates. We did see a hike in the last week of January. We think we see more, at least two or three more, in calendar year 2023. But some of these prices, labor and energy specifically, will be pretty sticky, will be hard to solve inflationary trends in those prices.

We know the federal bank really has one tool to use and one mandate, and that is interest rates in order to stabilize prices. We’re also seeing global economic growth struggle as population growth comes to a halt or even turns negative in places like China. That’s I think a big deal relative to the last couple of years when we were seeing population in China and other countries explode. Generally speaking, there will be fewer consumers over the next decade. Labor though does stay expensive because there are fewer workers, and those are two themes that we’re really focused on in the next couple of years.

We’re also seeing, once again, strength in the dollar and really weakness in other currencies. And that’s a big deal to us and we’re really focused on more of these currencies in emerging markets like Brazil, Argentina, and big importing places like Egypt, the Middle East. Purchasing power has eroded after two years of high prices, rising interest rates, struggling economic growth. We think that that weighs on demand expansion in 2023 and probably for a couple of years. We’ve also really eliminated the entirety of risk associated with war in Ukraine, the first land war in Europe in seven decades.

It was very, very bullish for a short period of time where there has been a willingness on behalf of importing countries, the United Nations, the International Monetary Fund, a lot of non-governmental actors, making sure that this Black Sea grain does get out of the Black Sea region at almost any cost. That has given the US competition for exports in the case of wheat and corn. In fact, Russian exports seem to have normalized completely, and so there’s really no risk today that importers can’t secure Russian wheat, which is very cheap, very abundant. That’s been a weight on the market. But one of our core thesis moving forward into 2023 as the growing season does lie just ahead is that La Niña is ending.

After three consecutive years, La Niña has been a real drag on global grain productivity growth, mostly in the form of excessive heat, in a lot of major exporting countries, but La Niña is dying currently. The best forecasters do expect El Niño to be established at some point in late spring or summer. We found that to be very, very good for weather across a lot of important parts of the Northern Hemisphere, including Nebraska and parts of Europe and Argentina next year. El Niño does continue into the autumn months. Argentina probably ends this period of three consecutive years of drought and extreme weather.

Odds are high that US corn, soy, and wheat yields are at or above trend in 2023. This could be the year that we finally break that 180 bushel threshold in terms of national corn yield, if that’s the case. That coupled with the lack of demand growth really does allow us to build stocks very, very quickly. We do though need to separate the short-term outlook from the long-term outlook. We’re still not terribly far removed from concern over global food shortages and what was deemed as something being very close to a food crisis. At this meeting 12 months ago, I think the entirety of the market was pretty bullish just seeing supplies run out.

We weren’t producing more of things. Inflation was intact and demand growth was intact, and that collided with supply issues and gave us very tight markets. We’re still not very far removed from that. Corn supplies are not abundant. Soybean and wheat supplies in the US are not abundant, and even the global market today is not terribly abundant in terms of supply. Based on hemispheric calendars and crop cycles, Brazil, which has stolen a lot of corn export demand from us, is now out of corn. Brazil corn last week traded up to $7.45 per bushel. Exports will be very, very slow. The corn market must contend with the absence of South American supplies for another three or four months.

I think these seasonal trends broadly will stay intact. However, I don’t think we need 40 or 50% rallies from harvest loads like we saw last year and the year before, but we do think that we stay in a range of $6.60 to maybe $6.90 or $7 until we know what the US has planted in both corn and soybeans and even spring wheat. Markets generally tend to move up, whether that’s on five or 10 year or 30 year seasonal trend. It’s very hard to dispute that. I guess what we’re concerned about and what our high level strategy, unlike the last two years, we want to use near-term strength to position for what could be a violent negative reaction come spring/summer if there are no weather threats in the US or elsewhere in the Northern Hemisphere.

We saw a pretty violent downward reaction last summer based on the Federal Reserve, central banks worldwide combating inflation. Generally speaking, we saw decent early season weather last year. Again, it’s the sort of June-July period that we do want to position for. Unlike last year, I don’t know if we’ll get major recoveries post-harvest if we do see that US corn yield from 180 bushels an acre. What got us here and, again, what is different from last year and the last couple of years and what we think will be the case this year is that we have seen six consecutive years that global grain productivity has been absent completely.

In the ’22 crop year, combined yield for corn, wheat, barley, sorghum, soy, and canola combined has really been unchanged from 2016. We have failed to grow productivity based mostly on Mother Nature and to some extent Russia’s invasion of Ukraine last spring. We’ve seen this plateauing of production. This has collided with what has been ongoing demand growth until now, and that has given us very, very tight balance sheets and due the effect of La Niña, I think. It started with Pacific Northwest and Canada two years ago when we saw consecutive days records being smashed, temperatures 110 to 120 degrees.

In this part of the world, the Northwest US and Southern Canada, that is 40 or 50 degrees above average. Heat inflation was the new normal and it was a big, big drag on global grain yields and global oilseed yields. This follows with 10 to 12 consecutive days last January where temperatures in Argentina were 105 to 115 degrees. This slide where you see the brown and purple, that really highlights the primary corn and soybean production region of Argentina. It was pretty dire. They’ve been trying to plant later and later to avoid heat, but that has been unavoidable now. We lose a lot of soil moisture very quickly as you guys are well aware of when temperatures are above 105 or even 110 degrees.

It’s very hard to combat that evapotranspiration. Egypt smashed all of those records the following spring. Last spring, temperatures in parts of India were 115 to 120 degrees. India lost about 20% of its wheat crop last year and that was after harvest. A lot of India’s wheat crop is irrigated and that water comes from the previous year’s monsoon. But after the crop was harvested and stored, it was so hot and so dry that we saw pretty major kernel shrinkage, to the point where we lost 15 million tons of Indian wheat production compared to initial estimates.

That was then followed by the hottest summer on record in Western Europe, which, of course, is a major corn producer, wheat producer, and barley producer. If you remember the tarmac at London Heathrow Airport melting last summer, London and a lot of other parts of Western Europe were very ill-prepared to deal with temperatures even above 85 or 90 degrees. This was pretty dire. We went months without rain in Western Europe. We keep adding to the list of these major producing and major exporting regions just losing lots of yield based on dryness and extreme record-breaking heat. Of course, the US joined what was a very bad party last summer, especially in the second half.

This shows us drought as of November, but we all know it was much, much worse in July and early August. Kansas, Elgin, Nebraska even, there is no way the US Weather Service could present drought being any worse since it was in the exceptional category. That is the last possible category. Drought during some parts of last growing season were the widest they’ve been since 2012. It was very, very difficult to grow and encourage plant health when there’s just no soil moisture, and it is 100 degrees or more for consecutive days. We went through several bouts of that West of the Mississippi last year.

Almost every major producing region, really everywhere except for Russia last year, experienced some kind of weather adversity. And that triggered fear in the marketplace of shortages. Demand was still growing. We saw this huge inflationary period over the last 12 months in corn, wheat, soybeans, really all raw materials combined. What changed though very quickly in the early part of last summer is when these food price indexes and inflationary measures got to a certain point. It does seem that once the FAO World Food Price Index reached 160, this crossed the threshold of comfort for a lot of banks and, of course, the consumer.

Very quickly, central banks acted, interest rates were put into place, demand slowed, and we’re starting to see a cool down in inflation in raw material prices, but what we’re concerned about is that this continues. We will continue to see central bank action as their mandate is to encourage price stability at almost any cost. The goal is to somehow encourage unemployment, encourage declining consumer spending just to cool down an overheated economy. The two sectors that we think will keep this period of interest rate hikes intact, the labor market and the energy market. In 2021 officially, the US population grew by just one-tenth of 1%.

That was the lowest in the history of record keeping in the United States. In 2022, it’s unofficial, but it is estimated that the US population grow by four-tenths of 1%, so some improvement. We’ve had this downward trend in tech now for many, many decades, really since World War II, but it’s crossed the level that we’re very, very concerned about future human beings being able to work in the United States. We think about the labor market even 10, 15, 20, 25 years from now, there would be fewer workers available. We’ve already started to see this contraction.

This qualifies generations, but for three years ending in 2019, we have seen the working age population gets smaller than it was the previous year, not larger. This is a big concern for the labor market moving forward. And already as you are well aware, unemployment in parts of the Central United States is already very, very close to 0%. None of this stuff improved, and there’s really not a good solution to this. We can talk about immigration reform. Excuse me. We have heard that finding workers in the ag industry specifically has been very challenging. There’s just less interest from Latin America in terms of people coming to work on farms.

It’s hard work. That along with just fewer workers in the United States, this is going to be a challenge for everyone moving forward. Labor costs will stay elevated. We don’t see a solution on the horizon. There will be an acceleration of technology and efficiency, but how fast that can offset a fewer number of people is yet to be seen. We didn’t want to communicate the labor cost specifically, probably stay pretty elevated for the next decade, two decades. The energy market has been pretty weak. We are concerned in the crude market that interest rates will continue to rise. We’ve had kind of a knee-jerk reaction to that with crude down to 73, $74 a barrel.

But until we encourage higher production to us, we don’t think that many of these issues or any of these issues will be solved. Some motor gasoline stocks in the latter part of January were down 4% from the previous year, the lowest level since 2014. Total crude inventories, this is what’s available to the free market and what exists in the strategic reserve, total just 820 million barrels. That is down about 20% from the previous year and down 27% from two years ago. We’re not sure how this is solved without buying more crude oil, whether that’s from our own supplies or from an OPEC producing nation.

When that’s the case, you have more buyers than sellers in the marketplace, that tends to be supportive of price, of course. We don’t know how to restock our reserves or replenish total crude oil supplies without price going up. Price also needs to go up to encourage production and exploration. We think that we’re in this new equilibrium price of maybe 70 to $90 crude oil. Diesel prices have come down, motor gasoline prices have come down, but I don’t think there’s much downside risk from current levels. Maybe we can lose note of three or 5% in diesel, but that is probably the lower end of fair value.

I’m not very insightful given that the last 15 years of 0% interest rates have been very rare in the history of time. As best as anthropologists can tell, over the last 5,000 years, interest rates have been about four to 6% for most of that time. Never have they been 0%, not even in the Great Depression. Thinking about interest rates, benchmark rates at three to 5% for the next couple of decades even is not terribly unique in the history of the world. Really what’s been more unique is 0% interest rates. We want the farming and the ag communities to be prepared for interest rates at the farm being between four and 6% through the foreseeable future.

While we’ve got demand growth slowing based on central bank policies and high prices, we are once again intend with currency issues. To us at AgResource, there is a lot of uncertainty about US and global economic growth moving forward. A lot of people have talked about this looming recession and deflationary period. To us, we just want to distill it into a few simple things. One is whether or not interest rates are going up or going down, and really currencies tell the rest of the story. One of our concerns after this two year bull cycle is that everyone else in the world economically is doing relatively poor compared to the United States.

That’s very positive for us or relatively positive, but that does give us very weak currencies in places like South America, North Africa, the Middle East. I was going through some kind of thought exercise, thinking about this and why this is so important to really the cash price of grain in Nebraska or in any specific region of the United States. If the Brazilian exporter can sell let’s say one bushel of soybeans to China for $15, the Brazilian exporter then takes that $15 since everything is traded in dollars and converts that then into its domestic currency. The US exporter let’s say does the same and gets $15 and puts it in its pocket.

The Brazilian exporter in 2016 would take that $15 and get about 45 Brazilian Reals. Today, the Brazilian exporter can sell that same bushel of soybeans to China for $15 and it gets about 70 Brazilian Reals. There’s some nuance to this, but we are seeing that margins stay in intact, even in bear market trends in places like South America because of currency weakness. I don’t think there’s anything to suggest that Brazil stops expanding its arable land, producing more, planting more, putting money into technologies, genetics. Brazil will be a powerhouse and competition for us for the foreseeable future and kind of act as a weight on the market moving forward.

High competition when we get currency relations like this. There’s also concern about demand. Now, let’s talk about Egypt specifically for this thought exercise. Egypt’s economy is doing pretty poorly for a long time now to the point where they asked for a loan from the International Monetary Fund worth $3 billion. The IMF said we’ll give you that $3 billion, but only if you allow your currency to float freely. You can do nothing to prop up your own domestic currency. And that happened about the middle of March 2022. You can see very easily what happened when Egypt’s Pound is allowed to float freely.

We’ve been through two major devaluations in the last 12 months, and now the Egyptian Pound is down about 49% from where it was in January of 2022. That’s significant. That really impacts negatively purchasing power parity. The exercise here then moves to let’s look at now the price of Chicago wheat, which is down about 3% from where it was in January 2022. But since Egypt has to take those pounds, convert them to US dollars to buy wheat, buying wheat in Chicago, for example, would cost Egypt about 63% more than they were paying in January 2022. We’ve heard in the news of the population struggle to buy bread.

There is unrest amongst the population, and now the World Bank is largely financing new food purchases in Egypt. That’s the good news is Egypt is getting the money to buy wheat. They just bought a lot of wheat this last week, in fact, but these large charitable organizations are having to get involved in Egypt’s food program is a little concerning to us in the long run. We’re just not going to see discretionary purchases of wheat or corn or vegetable oils or dairy products in a lot of North Africa and the Middle East. They will buy what they need and not much more. I don’t think this issue changes until these currency markets normalize.

When that happens, we’re really uncertain about. All of this, given two years of high prices, interest rates existing and getting higher, current seeds weakening, purchasing power there is declining, we have for the first time in decades, the USDA projecting pretty sizable global demand contraction. This is not just an idea from us, but rather the USDA and all their wisdom and all their budget and their PhD economists now project global corn demand declined about 19 million tons from last year. This is a level that we haven’t really seen in the past. Notice even in 2012, we saw very little change in demand. It was just that the US lost demand and instead it went to South America and Ukraine.

But this year it’s a worldwide phenomenon. This really does highlight and underscore that because prices are high, importer currencies are weak, we are seeing a lot less discretionary consumption in the world market. Seeing on balance the US exporting fewer tonnages and getting fewer dollars for our exports on a monthly basis. A year ago during the winter months, we had pretty sizable positive trade balances, but we have struggled to grow our positive trade balances since .we’ve seen pretty sizable negative balances in the first half and into October of 2022. This, again, is just giving us real data and telling us that the global purchasing of agricultural commodities is starting to struggle, which makes sense.

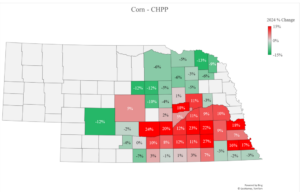

This is just the invisible hand at work. We’ve had 24 months of a real bull cycle, and that bull cycle is starting to fix some of these issues. Thinking about the future specifically, we have found ourselves internally at AgResource talking about things like moving corn from Illinois to places like Nebraska and Kansas to those flea markets there, the levels of various rivers, very nuanced things and things that are specific to grain traders. We’ve had to remind ourselves that not everyone will care about this, and that’s what we’ve seen in the speculative community. This shows us the graphic of index fund positions, so things like big retirement accounts, institutional investors.

You can see between 2020 and the middle of 2022, there was really fear over food, crises, shortages, weather issues, no interest rates. It was a very exciting market and a lot of money was put into the agricultural space. But since then, they’ve liquidated about 400,000 contracts. The ag sector is no longer one that includes people outside of ag specific traders, end users, and farmers anymore. Until we see the speculative community find a new story in the agricultural markets, we kind of lack that discretionary investment. I never think that fund positions or fund money flows impact price for any length of time, but it is nice to have new money coming into the ag space if we’re to stay ultra bullish in the long run.

This shows us what has happened with Russia in the Black Sea region, despite there being war, reputational issues in Russia, logistics issues in Russia. There’s been just such a willingness to find supplies within the Black Sea region on behalf of the World Bank, United Nations, importing countries, that this export corridor that was created in July has been fairly successful. Monthly exports in Russia in certain months, January included, was a record for that particular month. Despite all odds being against Russian ag exports, probably they will export a record or near record amount of combined agricultural products in ’22-’23.

This is very different than what everyone thought in March, April and May of last year when we thought maybe we wouldn’t get any wheat out of Russia or any corn out of Ukraine. But there has been enough interest in this and the corridor being established has been a pretty big deal. We were not a wheat exporter. We have not been a wheat exporter this year because Russia has abundant, very cheap supplies. We found that the Russian market and the Ukrainian corn market have just gone to levels that find demand no matter what. And that has been the template.

We could add a risk premium based on war if physical grain flows are disrupted, but that has to be the case to sustain new buying in the US ag markets. We don’t think that happens at least in the month of February. Russia and Ukraine are there with corn and wheat supplies. Since the Brazilian currency has been weak, there is new arable land, there is margin to be had, we’re going to see another 5% expansion in Brazil’s winter corn area. This shows us Safrinha corn seeding since 2000 and the explosion that occurred in 2012, which is another bull market that encouraged a lot of things. One of those things was really this newfound corn industry in South America, Brazil specifically, which has been ongoing.

We went to visit Brazil and went on a tour a couple of weeks ago and we met with one of the big state agencies in Mato Grosso. We asked them, if we are planting in Brazil only short season soybeans and this odd winter corn crop that can sometimes enter its critical growth stages after the wet season has ended there, what is the potential for growth moving forward in South America and in Brazil? Maybe it’s being capped by yield growth in soybeans and uncertain weather in corn.

But that fellow left the room when I asked that question, came back with his laptop, graphic that showed the state of Mato Grosso that there was a potential doubling of row crop production, and that’s just converting pasture land to soybeans and corn. What they found is a lot of that pasture land would be very high yielding corn and soybean ground in just a couple of years if it was converted. At the right price, Brazil can produce at least 30% more corn and soybeans over the next seven or 10 years. Like I mentioned before, we have to revisit this and this does act as a weight on rallies moving forward.

We’ve got to see supply dislocations if we are to stay bullish beyond spring or summer of this year. And to that end, we thought soybean crop looked very good, soil moisture was adequate, that crop very likely, and soybeans will be 153 to maybe even 155 million tons, so up something like 500 million bushels year over year. There are challenges harvesting the crop. It stayed a little too wet, but we are seeing harvest accelerate. The cash soybean market in Brazil start to weaken. We do know that there will be very little soybeans exported out of the US after about April or May, just a matter of whether Mother Nature can cooperate in the Northern Hemisphere.

And if it does, I think there will be bushels of soybeans without a home in the United States and probably in Brazil even. That crop will be so large. Unlike last year and the year before, the soil moisture is more than adequate in Brazil currently. Most likely we will see a total Brazilian corn crop of 125 million bushels, I’m sorry, 125 million tons, so up a couple hundred million bushels from last year. It was very clear to see that once that crop was harvested in Brazil, the US export program all but shut down in summer and early autumn. We’re concerned that that happens again.

There’s this major shift in global trade flows where Brazil dominates feed exports and the US loses its market share May-June onward. Ukrainian corn is still very cheap. As far as we know, stocks have not been fully depleted. It’s been odd. We thought briefly that Ukraine corn would not be available. And for a certain period of time, it wasn’t. But once the export corridor was established and determined to be successful, Ukraine corn is now selling to the importing markets at just 20 cents over the Board of Trade, whereas you can see the US and South America are about $1 to $1.20 per bushel over the Board of Trade.

Ukraine is by far the world’s cheapest source of feed grains. With that said, talking about Europe’s crippling drought this summer, and we thought that would be a big driver of feed grain supply and demand tightness moving forward. But oddly again, since there is war in Ukraine, Europe has access to this fairly sizable and very cheap supply of corn in Ukraine, to the point where imports of corn into Europe are up two or three times from last year and that market is all of a sudden oversupplied. We can check that off of the risks of tight global supplies. Europe has had access to adequate amounts of corn despite having crippling drought.

Cotton is not a big issue in Nebraska, nor are oats. But we look at these markets just to see what happens when prices get too high and the supply and demand issues start to be solved. Cotton, which was priced at a near record level, since then, the last three months, the USDA has been forced to lower global cotton demand by about seven or eight million tons. By doing that, when we exclude China, all of a sudden, cotton stocks to use, which is what determines price, is at the second-highest level on record. The cotton market has lost about 50% in value over the last 90 days. It’s been a rapid shift, and it shows us how these markets can solve supply issues.

We’re to the point in the cotton market where maybe that market is not going to compete or participate in this battle for acreage this spring because we don’t need to find cotton expansion. That market is adequately supplied both the US and in the world. Oats, similar. We look at a market that really doesn’t have any demand growth and hasn’t had demand growth for a long time. We feed some to animals. Domestic human food consumption’s been pretty stagnant. While it appears that oats also participated in this cyclical bull market in the world of agriculture, all that really happened was that we had a very bad Canadian crop in 2021 and a very good crop in 2022.

The market was forced to add premium because of supply loss, but then extracted all of that premium very quickly once that supply returned. Not that this happens in corn over the next six months, but we are thinking something like this happens. If we’re not seeing demand growth in the US, weather normalizes and we produce a big crop, there’s just no reason to have substantial premium in the market. Does the corn market in the long run, over the next 12-16 months, have to go in search of world market share? And that is one of the fears or one of the risks that we think the markets face over the next several months, several quarters.

Butter is another market that we can see and feel the invisible hand at work. We know that butter consumption, a majority of us use during the holiday season, family get together. It’s holiday baking. In the middle of 2022 when stocks were down 20 and 30% from the previous year, production was also down. We were concerned that we would not have enough butter to supply that holiday seasonal demand. But when butter rallied to an absurd price, on certain days last year, it was $3.40 to $3.50 per pound, by far a record, but you can see in the graphic on the right what $3.50 butter does to supply and demand, and very quickly we found production growth.

We found demand destruction, to the point where at the end of the year, butter stocks were up 9% year-over-year, and the butter market has dropped from $3.50 to now about $2.30 per pound. Again, this just shows us how the invisible hand works and how in the world of agriculture it can work very quickly. And that that is the goal of the market and that’s kind of what we’re seeing in a lot of these markets, specifically cotton, butter, oats. Does this begin to impact corn and soybeans in the long run? We think that is a risk that the producer faces in calendar year 2023.

A lot of this outlook too and that managing risk I think implies now selling rallies in the next 30, 60 and 90 days instead of buying breaks is weather forecasts six and eight months from now, but we think odds are high that Midwest Central Plains weather improves, and we don’t see extreme heat and dryness like we saw last year. That’s basically on a shifting ocean temperature anomalies. Now, this graphic shows us La Niña in the blue, red is El Niño. This maps just ocean temperature anomalies in this small region of the Pacific.

But we have determined that this small region of the Pacific, weather is cooler than normal, La Niña, or warmer than normal, which is El Niño, does impact significantly a lot of global weather patterns, most significantly in Australia, Argentina, East Asia, and the Southern US, but it does start to have pretty considerable effects outside of that, including a lot of the US and a lot of Europe and the Black Sea region. This is a forecast from the Australian Bureau of Meteorology, and they are the best at doing this, because El Niño and La Niña most considerably impact weather and really food supplies in Australia.

They’ve gotten very, very good at monitoring this data and making forecasts over the next six and eight months. Anyway, the Australian Bureau of Meteorology does think pretty confidently that we will see an El Niño trend by May, an ocean temperature warming into the summer and autumn months. That is a long-term forecast. We are seeing the Pacific Ocean warm pretty rapidly on a daily basis currently. This shows you the daily temperature changes. We’re at the point where La Niña is very close to dying outright and El Niño, as forecast by the best in the business, is probable by late spring or summer.

Why we’re concerned with that is if we just put El Niño summers against soybean and corn yields, we found odds of very good we will beat or exceed trend. We’ve spent a lot of work. We’ve got offices in Europe and South America. We spend about 400 man-hours just monitoring five or six markets, but this is still more or less predicting the future. When you see odds like this, you pay very, very close attention to them. We think that soybean production could be up at minimum 100 or 150 million bushels in 2023. Corn production could be up by 500, 700 million or even a billion bushels in 2023 if we do see five or 10% yield growth relative to trend.

Thinking about a 10% boost from trend in national corn yield this year, that would give us about 190. It sounds absurdly high, but we did want to communicate that very likely we’ll have a mild summer, pretty wet. I remember most vividly 2009 when it was just cool and wet all summer, it was very difficult to plan outdoor activities, but it’s very, very good for crop health. We do think that odds are the best they’ve been in years that we will see trend yield at least, and so that gives us 180 bushels nationally for US corn yield. Forecast six months in advance, but we are starting to see some of this happen.

Drought very quickly has been eliminated East of the Mississippi River, specifically in the Delta, Southeast and Mid-South where crops will be planted first. It is still very much winter in the principal Midwest and in Nebraska, but early corn planting will start in Louisiana, Texas, Southern Mississippi during the last week of February. March is a very big month for the larger producing regions of the Delta and Southeast. We’re not very far removed from that. Soil moisture is adequate to surplus in those regions. We don’t think there will be many problems at least for the first half of the growing season there.

We’ve also seen major drought improvement in the West Coast, including California, which just might for the first time since 2017 experience only very light drought or no drought at all. Those forecasts are for additional moisture improvements. 30 day, three month drought outlooks really keep drought confined to the spine of the Central US, which unfortunately does include Nebraska, Kansas, Western Iowa. But we’re hopeful that this El Niño pattern will on the margins start to ease drought by late spring and the early part of summer. I wanted to highlight California. This shows us 30-day percent of normal rainfall or precipitation.

Already in the Sierra Nevadas, there are 30 to 35 feet of snow present. That’s about 350 to 400 inches. That’s already more than what they get through the entire winter or only half through winter in the mountains of California. We mention that because I do think farmers in places like Southern Oregon, Nevada, California will have their full water allocations for the first time in many years. California is a top food-producing state, so almonds, tomatoes, wheat, even some corn probably do much better in terms of yield and production. Dairy markets too will be subject to larger per cow output in that part of the world just based on favorable weather and favorable moisture reserves.

We put all of this together in what we think new crop balance sheet, and we can even assume the USDA is correct with its old crop forecast of about 1.26 billion bushels then stocks. But since we’re not growing demand meaningfully, in fact, looking at 2022 US corn consumption, we’ll be down about a billion bushels from the previous year. It really comes down to China not buying corn, whether because they don’t need it, or they’re getting it from Ukraine, or these growing US-Chinese tensions. But for whatever reason, it doesn’t really matter. We’re not growing total US corn consumption.

If we do find any measure of acreage expansion, we see a trend yield of 181 bushels an acre, and we’re left over with something like 2 billion bushels of in stocks, even assuming something like normal growth in ethanol, some boost in export demand, but we will have more corn without a home than we’ve had in recent years. Our work would put about two billion bushel in stocks at $5, $5.30. Therein lies the risk at harvest, at least to us. This will not be terribly precise and it’s fluid and we will adjust these numbers on a weekly and monthly basis throughout the growing season and based on what we see in the export and ethanol markets.

But one of these numbers has to change pretty significantly to prevent building stocks in ’23-’24. The way we see it for now and what strikes us the most is that this issue is solved in just one crop year because of yield growth and a lack of meaningful demand growth. Soybeans look similar in that we’ll be building stocks, not decreasing stocks if weather cooperates, which most likely it does, and we see a trend yield of 52 bushels an acre. There will be growth and crush, but we don’t think there’ll be much growth in exports based on Brazil’s monster crop of 153 to 155 million tons, which will extend their export season into December-January of next year if you know normal consumption trends stay intact for soybeans globally.

Just as a thought exercise, let’s assume they get that 5% yield jump from trend and we’re left with 185 bushel and acre yield. We’ve got in stocks over two billion bushels and we have to find demand. This assumes much larger feed use, larger ethanol use, and a little bit higher exports and higher world market share, and yet we’re still left of two billion bushels. I do think that if Mother Nature is kind to us in June and July, something like let’s call it conservatively 1.7 to 2 billion bushel in stocks seems somewhat inevitable. The market will be resetting based on the lack of demand growth, adequate supplies.

There are markets though that we do think continue for another couple of years, and that is vegetable oils, US soybean oil specifically, and the livestock markets. Red meat supplies specifically are going to be challenging to keep above domestic consumption without massive growth in the beef cow herd, which will be difficult because of interest rate uncertainty and current weather, forage feed availability currently. When soybeans, we’ve talked about renewable diesel, and this is all we got about 12 months ago. We knew it was coming. We knew it was something that was chemically identical to diesel. There’s really no restrictions on engine usage.

There’s a lot of hype surrounding this. We didn’t have any data to measure this, except for this one chart which the EIA told us that production of renewable diesel would increased by something like eight times in a matter of two or three years. Doing the math on this, we thought we’d have to grow something like 10 or 15 million additional acres of soybeans to produce enough feedstock to meet this, which is still the case we think. I don’t think that really occurs and we do run out of feedstock and that’s what caps this industry. But what matters most is that it looks like this graphic will be proven correct.

We’re seeing just every week new plants being announced that are being built or being retrofitted. In a sense, these are refineries and soybean crush facilities. What is unique about this is that unlike the 2005 RFS and the ethanol boom, this is not going to be driven by farmer owned co-ops or even federally mandated production and consumption. This is mostly due to state tax credits, but I think that’s just a small part of it. I think a large part of this is consumer preference and this quantifiable premium that the private sector is being put into being green. Think about United using sustainable aviation fuel, renewable diesel being delivered all over the world at this point.

Also, the participants in this, unlike farmer co-ops, these are the major petroleum companies like British Petroleum, Royal Dutch Shell, Phillips 66, Marathon, et cetera. The combined market cap from these companies at about $1 trillion or more. Even if this were to lose money in the short-term, that is not going to impact BP’s bottom line really at all. They are committed to doing this, at least for now. It does look like they are going for that EIA planned capacity expansion graphic. Ultimately, we started to get data. The EIA did create us a monthly data series, and you can see that it has exploded just as it was projected to. Renewable diesel production in 2022 doubled from the previous year.

Once a year, we get production capacity updates based on what’s being built or planned to be built production capacity for renewable diesel will double again in calendar year 2023. We are going to be crushing soybeans for the first time in I think the US history for oil and nut mill, which makes us long-term bearish of mill, but I think very bullish of soybean oil and other vegetable oils. There’s no doubt we are going to be crushing those soybeans. This shows us actually what crushed margins are in Central Illinois as of the end of January. It’s $3.45 per bushel. Every bushel crushed is given $3.40 total revenue. You can see what’s happened with the advent of this renewable diesel industry.

On average, we see on a monthly basis crush margins at $1.10 to $1.50, maybe $1.60 per bushel. But in the last 18 months, we have seen margins as high as $4, $5 per bushel. The market is clearly trying to produce incentive to maximize crush, and we will be crushing that for vegetable oils because of its budding renewable diesel industry. This happen in real-time in the marketplace. Soybean oil exports so far this season for all intents and purposes has been zero. This graphic shows us soybean oil export sales cumulatively as percent of the USDA’s forecast. You can see very clearly we’re not exporting any soybean oil.

I don’t think that’s because there’s no demand for soybean oil, but rather the domestic market is working very, very hard to keep all of that supply at home. It maybe the case that we don’t export much if any soybean oil at all this year, but that is because it is all being absorbed by the domestic market. The next big bull market is in cash cattle and I think red meat. The select beef cutout in late January was the second-highest on record at $255 per hundred weight. The January Cattle Inventory Report showed us that total cow numbers are just below 29 million head, which is the lowest since 1964.

The beef heifer replacement herd was down 6% from last year and is the lowest in the USDA’s data series, which started in 1963. Livestock prices are going to go up, and the goal of the livestock is to find a price that encourages acre or herd expansion in spite of interest rate uncertainties, low forage feed availability currently. In spite of all of those obstacles, the market does have to find a price that encourages herd expansion. We think this will take a couple of years to fully replenish the cattle market. It just shows you how dire the situation has become in the last three or four years and how quickly the beef cattle herd has changed since about 2019 or 2020.

We don’t think this expansion happens in the rest of winter or spring. What does the market do with this over the next couple of years? The USDA has also told us that feeder cattle values in the fourth quarter of this year will be $224 per hundred weight. There are still upside risks in the livestock markets we think. That is where we are. These bull markets tend to last anywhere from three months to 24 months. Let’s call anything above 4.50 corn a bull market, and so we are in our 24th month currently. We don’t think that this thing has enough fuel to sustain itself beyond the spring or early summer.

Again, we wanted to communicate to you that there is risk that these markets reset thereafter. We want to use the next three or four months of potential seasonal market strength to position correctly for harvest. As usual, thank you for your time. I know you guys are the busiest, hardest working people on Earth. If you have any questions about anything, please reach out to the Mid-Plains team or my email addresses here and please don’t hesitate to send me a note with risk management issues or market issues at any point in the future. Again, thank you for your time.